Capital Debt Policy

1. Contents

- Overview

- Objectives

- Framework for Managing Capital Debt

- Definition of Debt

- External Debt

- Internal Financing

- Process for Prioritizing Capital Projects

- Table of Evaluation Criteria for Capital Projects

- Internal Loans

- Incurring External Debt

- Metrics on Debt Affordability and Debt Capacity

- Key Ratios

- Other Metrics

The University of Guelph has established an Integrated Planning process that supports the University’s mission and strategic planning directions. The outcome of that process is a five-year Integrated Plan that contains key goals and initiatives that help determine the University’s priorities in making major resource allocation decisions.

Within the Integrated Plan are identified two broad capital expenditure objectives, the need to address deferred maintenance and the opportunities that cost-effective investments in buildings, equipment and support facilities can bring towards meeting the University’s goals. As a result, with the traditional sources of government capital funding shrinking, the use of the University’s debt capacity plays a critical role towards meeting the goals of Integrated Planning and therefore the likelihood of the University achieving its mission.

The objectives of this policy are to:

- Define a framework within which University debt is incurred.

- Establish a control framework within which debt will be approved and managed.

- Establish debt management guidelines.

The following will be used in the consideration of all new capital debt:

- Capital debt is a valuable resource that can advance the success and sustainability of the University however capacity to incur and service debt is limited.

- An objective is to maintain or improve the University formal credit rating. Debt management is a key consideration toward achieving that goal.

- The University will not incur long-term debt in direct support of operating activities. Any long-term debt must be in support of capital projects that maintain, enhance or create physical assets.

- No college, division, fund or agency of the University may incur debt. All debt used for the benefit of any college, division, fund or agency must be approved under University’s Board of Governors approved policies and processes.

- The first priorities for funding capital projects are capital grants, project-derived operating revenues, or realized donations that reduce financing requirements.

- Where a fund-raising target has been set, 75% of that target must be received before the construction project can be started.

- Any debt will have an identifiable source of servicing including repayment as a condition of approval. This applies to non-amortizing debt in which case an internal sinking fund must be created.

- Access to University debt is not an entitlement. Allocation of debt must be made to those projects that contribute most to achievement of the University’s mission and goals.

- Debt will be allocated based on projects which have been evaluated using the consistent and documented criteria.

- Monitoring debt, in the context of overall University financial health will be achieved using a series of metrics that will be compiled and reported to the Board annually.

- This policy will be reviewed by the Board at least once every five years.

Universities as with most organizations may draw on both external and internal cash resources to finance projects over various periods of time. For the purposes of this policy both external and internal sources of financing will be considered debt.

External Debt

There are many different forms of financing and many different arrangements for providing lenders with some form of security for their funds. There are complex commercial transactions that have the appearance of having no obligations on an organization’s balance sheet (sometimes referred to as “off-balance sheet”). Most of these financial arrangements contain commitments for cash outflows by an institution to a third party for a period of time usually associated with the acquisition or use of an asset. For the purposes of this policy, external debt will include any type of capital obligation to a third party, secured by the credit of the University.

Internal Financing

The University normally has a positive cash flow generated within a variety of funds and generated from a number of operations. The underlying sources of this cash flow may be from the timing difference between the receipt and disbursement of funds e.g., deferred revenue, positive fund balances or from accumulated unit savings e.g., unit carry-forwards or central contingency funds set aside for future purposes. University pension plan and endowment fund investments are excluded as a source of capital financing.

In considering sources of capital financing, the University may allocate a portion of this cash flow essentially as temporary internal loans. The use of internal funds is normally limited to smaller projects with shorter amortization periods than external debt.

6. Process for Prioritizing Capital Projects

The University has limited debt capacity determined by both credit rating and financial sustainably objectives. It is therefore essential that the University carefully ration the allocation of debt to capital projects.

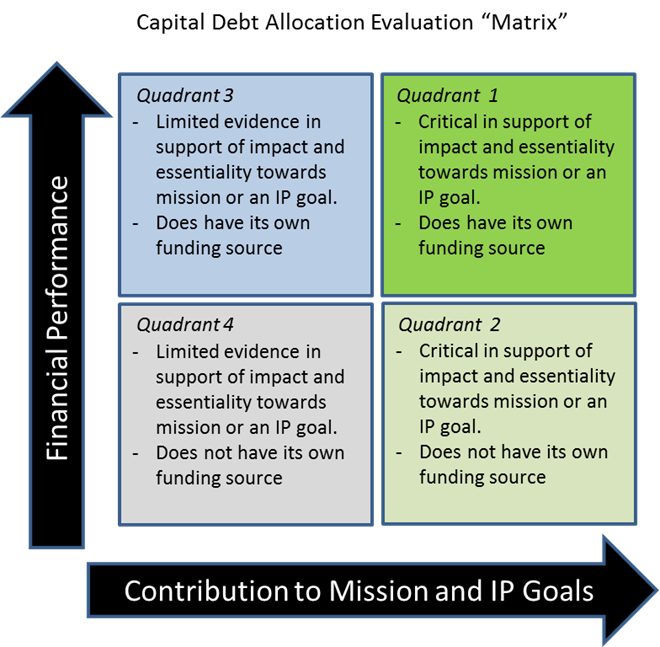

To assist the process, the framework in which capital financing decisions are made must balance risks and cost with the benefits of the project and include a clear and feasible plan to support the complete servicing (principal repayment and interest costs) of debt. The following diagram presented in the form of a matrix establishes the framework for evaluating capital projects. (a more structured assessment process will be developed to facilitate placement of projects within this framework).

As the matrix shows there are two major axes:

• Contribution to Mission and IP Goals; the extent to which the project is supportive of the University’s overall mission and how well it can map on to one or more of the goals as defined in the University’s Integrated Plan.

• Financial Performance; the extent to which it will not rely on current University MTCU Operating funds to support either its debt servicing requirements and if applicable, new operating cost.

The four “Quadrants” have been created to show the general boundaries in which a project may land. In reaching a conclusion as to where to place a project, more specific evidence-based “criteria” should be used. The Table below presents some key criteria that will be used in the evaluation of any capital projects that requires debt financing.

Table of Evaluation Criteria for Capital Projects

|

Criteria |

Description |

Evidence/Metrics |

|

|---|---|---|---|

|

1. |

Quality Improvement |

Describe the program that this project will support. How well does the project demonstrate improvement in a University program? This could include improving both program inputs and outcomes. |

Provide measurable and verifiable metrics that can support the achievement of the criteria. |

|

2. |

Productivity Improvements |

This should be mainly a quantitative assessment of the changes that the project will have on program productivity. Productivity can be defined as greater/more deliverables for the same cost or less. |

Provide measurable and verifiable metrics that can support the achievement of the criteria. |

|

3. |

Funding Sources (grants, donations, net revenues |

This should be mainly a quantitative measure and could be a combination of any direct increase in revenues and/or decrease in costs that the program will generate. Some projects are not specifically designed to generate revenues but may contribute to significant cost avoidance or reduction. |

Verifiable net operating revenues that support both incremental project operating and debt servicing costs; confirmed targeted capital grants; 75% of targeted donations received. |

|

4. |

Essentiality and Support of the University’s mission |

This will be a mainly qualitative assessment that should clearly map the value of the project to supporting or helping advance the University’s mission. Linking project’s outcomes to the Integrated Planning goals is a requirement. |

Evidence is mainly qualitative but clarity and relevance of representations will be important. |

|

5. |

Impact on Financial Health Ratios |

The University has a number of major Financial Health ratios that track important measures of financial capacity and performance. The impact of capital projects and related debt on these metrics will be an important consideration. |

Objectives are to maintain these ratios within certain ranges. (Refer to section 9) |

|

6. |

Risk Assessment |

The analysis for projects contains assumptions that reflect uncertainty e.g., costs estimates, financing sources, and revenue projections. The degree of risk underlying these assumptions is an important consideration in evaluating projects. |

Evidence can offset risk to a large extent. In addition, mitigation of risk can be identified and used as a distinguishing criterion between projects. |

7. Internal Loans

Available internal operating portfolio cash balances may be used to temporarily finance capital projects. While not formal debt, the use of short term internal operating cash to finance capital projects must be carefully managed to ensure liquidity in meeting operating cash requirements. In using these internal funds for capital project financing the following guidelines will be used:

1. Internal loans may only be sourced from the University expendable operating portfolio. University endowments and pension investments are excluded as sources.

2. The use of internal loans cannot compromise the operational liquidity requirements of the University. The University will maintain sufficient liquidity to meet at least 60 days of operating cash, defined as all non-endowment cash, maturing investments, and pooled funds convertible to cash, and can issue internal loans as a financing option so long as this level of liquidity is maintained.

3. Total outstanding internal loans should not exceed 50% of the University’s total expendable operating portfolio as determined at each year end, and if it expected that this limit will be exceeded it must be disclosed to the Finance Committee for discussion. Financial Services will monitor internal loans and report the total outstanding balance relative to the expendable operating portfolio, annually to the Board of Governors.

4. All internal loans will have amortization schedules for repayment with terms not exceeding ten years and under no circumstances can exceed the expected useful life of the project. There is no penalty for early repayment and internal loans will not be refinanced under normal circumstances.

5. The internal interest rate is set based on the Government of Canada Benchmark Rate plus the Applicable Credit Spread.

The Government of Canada Benchmark Rate is the yield published by the Bank of Canada for Government of Canada marketable bonds for the applicable maturity.

The Applicable Credit Spread is initially set at 50 basis points for loans up to 5 years and 75 basis points for loans longer than 5 years and up to 10 years. Financial Services will set the credit spread rates at least annually to reflect current credit and economic conditions.

6. All single internal loans greater than $2 million must be approved by the Board of Governors.

7. Cash advances from internal funds, may be advanced to finance projects until external financing is obtained. In these cases any advanced funds will be charged to the project at an internal rate of interest taking into consideration the term and the costs of advancing the funds to the total University cash flow.

8. Incurring External Debt

The following guidelines will be used when incurring external debt

Fixed Versus Variable: Lower financing costs may generally be achieved by accepting some interest rate risk through the use of variable rate debt, generally defined as debt with an effective term of one year or less and fixed rate debt, one year or more. The purpose of using a portion of floating rate debt for capital purposes is to lower the overall costs of borrowing, however, it is recognized that floating debt carries with it risk. The purpose of the following ranges is to define acceptable levels of exposure to both floating and fixed debt. The University will manage the percentage of fixed rate to variable rate external debt within the following ranges:

|

|

Maximum |

Minimum |

|---|---|---|

|

Variable Rate Debt |

40% |

0% |

|

Fix rate Debt (term greater than 1 year) |

100% |

60% |

1. Interest rate swap agreements may be used to manage the mix between variable and fixed rates on the University's external debt.

2. The University will seek to borrow funds from external financial organizations in an effective and competitive manner.

3. Term loans shall be used instead of demand loans wherever possible and whenever possible, loans shall be made on an unsecured basis.

4. Mortgages will not be given except for residence related debt respecting all covenants on existing debt obligations.

5. Although no specific limits are set, the University should obtain funds from a number of different institutions sufficient in order to avoid undue influence of any single lending source.

6. All loans shall amortize principal repayments. In the case of non-amortizing loans, an internal sinking fund shall be established with the objective of retiring the principal owing at or before the end of the term. In cases where the term is less than 25 years and the related capital asset(s) have expected use lives of 25 year or more, the sinking fund term may be extended to 25 years (essentially refinancing the portion of debt not covered by the sinking fund after 25 years).

9. Metrics on Debt Affordability and Debt Capacity

In assessing both its current and planned levels of debt the University will consider both debt affordability and debt capacity. Debt capacity focuses on the amount of leverage in terms of debt funding relative to the University’s total capital (net assets) and debt affordability focuses on the University’s ability to service its debt through operating activities recognizing strength of net income and cash flows. Two key ratios will be used to monitor debt in these terms, supplemented by additional ratio’s that can assist in assessing the impact of debt on credit ratings and may provide further comparability with other universities.

The metrics are targets established to manage debt, over time. They do not establish “hard caps” beyond which debt will not be incurred. To do so would first not be practical as metrics are historically calculated, subject to annual volatility and cannot be accurately predicted. In addition the evaluation of a specific project’s financial return and/or demonstrated support for the University mission must be a key consideration when making any borrowing decisions. For example a project that can demonstrate major revenue potential and support of the University’s core mission may be considered even if projections suggest metric target levels may be exceeded, in the short term. Conversely, having “room” to borrow should not be a signal to incur debt for projects that do not present sound fiscal and goal-related returns.

Key Ratios

1. Viability Ratio

Debt Capacity is derived from the balance sheet and generally is measured with a “Viability Ratio” calculation;

VIABILITY RATIO = Expendable Net Assets ÷ Total External Debt >0.65

“Expendable Net Assets” is defined as all internally restricted net assets plus internally restricted endowments plus unrestricted net assets. Unrestricted net assets will be adjusted to remove the accounting accrual for post-employment benefits. This adjustment is based on the non-cash nature of this adjustment and the current levels of volatility in the calculation.

Total External Debt does not include internal loans as these are accounted for under internally restricted net assets and to include them would result in a double counting of their effect.

2. Total Debt Service to Operating Expenses

Debt affordability attempts to measure the extent to which debt and debt servicing is a portion of University of total operating expenses. The greater portion that debt and debt servicing has of operations the greater the risk

DEBT SERVICING BURDEN = Debt Servicing Costs ÷ Total Operating Expenses <5.5%

“Debt Service Costs” are defined as all interest and principle repayment internal or external including any internal “sinking fund” payments.

“Total Operating Expenses” are total University expenses less capital asset amortization, less research and trust expenses plus principal and sinking fund payments.

Other Metrics

3. Interest Burden Ratio

This is a ratio used by many other universities and currently, by COU, to capture the interest only portion of capital financing. A measure of affordability, it is similar to debt service burden but can be used for comparability and tracking interest rate impacts over time.

INTEREST BURDEN = Total Interest Expense ÷ Total Operating Expenses <4.0%

“Total Interest Expenses” are defined as all annual interest payments, internal or external.

“Total Operating Expenses” are total University expenses less capital asset amortization, less research and trust expenses plus principal and sinking fund payments.

4. Debt Coverage

The ratio compares annual operating results, expressed in the form of adjusted net income, to total debt service requirement. Although particulars may differ slightly among firms, the approach is used in the credit rating process.

DEBT SERVICE COVERAGE = Adjusted Net Income ÷ Debt Service Costs >1.5x

“Adjusted Net Income” is defined as total revenue less amortization of deferred capital contributions less expenses plus capital asset amortization plus interest costs.

“Debt Service Costs” are defined as all interest and principle repayment internal or external including any internal “sinking fund” payments.

5. External and Total Debt to FTE

External Debt to FTE is a common ratio that simply divides total capital debt by the total number of student full-time equivalents (FTE). It is used by both other universities and credit rating firms. While neither a measure of debt capacity nor affordability, it is a consistent and easily calculated comparator. Total Debt to FTE is similarly calculated to the External Debt to FTE ratio, however, it includes internal loans to external debt.

DEBT TO FTE = External/Total Debt ÷ Total Student FTE <$10,000